Commercial real estate investment holds immense potential for generating substantial returns over time. Beyond rental income and property appreciation, savvy investors employ various strategies to optimize their returns. One such strategy that often goes underappreciated is leveraging commercial real estate depreciation for tax benefits. In this comprehensive guide, we’ll explore how strategic depreciation can bolster your investment returns and enhance overall profitability.

Understanding Commercial Real Estate Depreciation

Depreciation, in the context of commercial real estate, refers to the gradual decrease in the value of a property over its useful life. Unlike many expenses, depreciation is a non-cash deduction that allows property owners to account for the wear and tear their property experiences over time. This depreciation expense can be utilized to offset taxable income, thereby reducing tax liabilities and enhancing cash flow.

Factors Influencing Depreciation

Several factors influence the calculation of commercial real estate depreciation. These include:

- Property Cost: Depreciation is calculated based on the initial cost of the property, excluding the value of the land. This cost includes not only the purchase price but also any expenses incurred for improvements, renovations, or additions.

- Useful Life: The IRS sets the useful life of commercial properties at 39 years for depreciation purposes. This duration represents the period over which the property is expected to generate income before reaching the end of its depreciable life.

- Salvage Value: Depreciation calculations also consider the property’s estimated salvage value at the end of its useful life. This represents the residual value of the property, which may be minimal after decades of use.

- Depreciation Methods: Property owners can choose between different depreciation methods, such as the straight-line method or accelerated depreciation methods like MACRS (Modified Accelerated Cost Recovery System), each with its own implications for tax deductions.

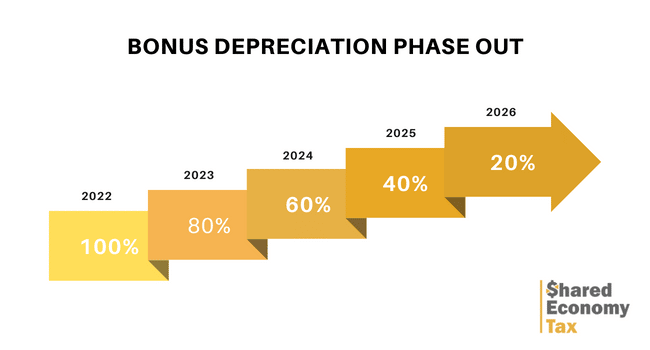

Total Cost of Ownership reveals a massive tax advantage when separating pavement from the main structure. While a commercial building depreciates over a tedious 39-year cycle, a $100,000 investment in asphalt qualifies as a “Land Improvement.” Under the MACRS system, this asset is recovered in just 15 years, though the real magic happens with immediate expensing. If the project qualifies for 100% bonus depreciation, you recover your accounting investment in year one. It provides instant cash flow relief.

Benefits of Strategic Depreciation

Strategic utilization of commercial real estate depreciation offers numerous benefits for investors:

- Tax Savings: By reducing taxable income, depreciation allows investors to lower their tax bills significantly. This tax savings can free up capital for further investment or reinvestment into the property.

- Enhanced Cash Flow: Lowering tax liabilities through depreciation can result in improved cash flow, as more funds remain available for property maintenance, debt service, or distribution to investors.

- Deferred Taxes: Depreciation can also be used to offset gains realized from the sale of the property. By deferring taxes on capital gains, investors can retain more capital for reinvestment or diversification into other investment opportunities.

- Asset Protection: Leveraging depreciation can enhance the overall return on investment (ROI) by providing additional protection against market fluctuations or economic downturns.

- Strategic Planning: Incorporating depreciation into your investment strategy enables you to make informed decisions about property acquisitions, renovations, and dispositions. By understanding the tax implications of depreciation, investors can optimize their investment portfolios for maximum profitability.

Strategies for Maximizing Depreciation Benefits

To maximize the benefits of commercial real estate depreciation, investors can employ the following strategies:

- Cost Segregation Studies: Engage qualified professionals to perform cost segregation studies, which identify and reclassify assets within a property to accelerate depreciation deductions. This can result in significant upfront tax savings and enhanced cash flow.

- Timely Renovations and Improvements: Implementing renovations or improvements to the property can increase its depreciable basis, thereby maximizing depreciation deductions. Strategic timing of these activities can further optimize tax benefits.

- 1031 Exchanges: Utilize 1031 exchanges to defer taxes on capital gains from the sale of a property by reinvesting proceeds into a like-kind replacement property. This allows investors to preserve capital for future investments while maintaining continuous depreciation benefits.

- Professional Guidance: Consult with experienced tax advisors, accountants, and legal professionals specializing in commercial real estate taxation. Their expertise can help you navigate complex tax regulations, identify opportunities for tax optimization, and ensure compliance with applicable laws.

- Portfolio Diversification: Diversify your commercial real estate portfolio to spread risk across different asset classes, markets, and property types. This not only mitigates risk but also provides additional opportunities for depreciation benefits and overall portfolio growth.

Technical Classification under IRS Publication 946

To master tax optimization, it is imperative to consult IRS Publication 946, which establishes the definitive rules on how to depreciate property. The code specifically classifies parking lots, sidewalks, and drainage channels as “Land Improvements,” granting them a 15-year recovery period. This distinction is critical for Cost Segregation strategies. By breaking these assets down from the overall building value (39 years), owners can legally and aggressively accelerate deductions. It is not just about asphalt; it is a technical reclassification that shields your capital from tax erosion.

Total Cost of Ownership (TCO) and Tax Impact Analysis

Total Cost of Ownership reveals a massive tax advantage when separating pavement from the main structure. While a commercial building depreciates over a 39-year cycle, a $100,000 investment in asphalt qualifies as a “Land Improvement.” Under the MACRS system, this asset is recovered in just 15 years, though true efficiency lies in immediate expensing. If the project qualifies for 100% bonus depreciation, you recover your accounting investment in year one. This provides instant cash flow relief compared to the slow amortization of the building itself.

Maximizing the Performance of Your Commercial Asset

Strategic utilization of commercial real estate depreciation is a powerful tool for maximizing investment returns and enhancing profitability. By understanding the factors influencing depreciation, leveraging tax-saving strategies, and seeking professional guidance, investors can unlock significant value from their commercial real estate holdings. Whether through tax savings, enhanced cash flow, or deferred taxes, strategic depreciation plays a vital role in optimizing investment performance and achieving long-term financial success in the dynamic world of commercial real estate.

Invest wisely, leverage depreciation strategically, and watch your commercial real estate investment returns soar.

Frequently Asked Questions (FAQ)

General Questions About Our Professional Services and Project Execution

Bonus depreciation allows commercial property owners to immediately deduct up to 100% of the cost of land improvements, such as asphalt paving, in the first year of service. Under IRS Publication 946, assets like parking lots and sidewalks are classified as “15-year Land Improvements,” enabling accelerated capital recovery that significantly boosts cash flow compared to the standard 39-year structural depreciation. A $100,000 investment in asphalt can result in an immediate tax deduction of its full value, providing a massive upfront liquidity injection.

Qualifying assets include asphalt infrastructure, lighting, and exterior equipment, each categorized under the MACRS system to maximize immediate tax returns. Precise classification allows for faster deductions based on the specific component’s useful life:

Minor Equipment (5 years): Bollards, reflective signage, and electric vehicle (EV) charging stations.

Land Improvements (15 years): Asphalt paving, concrete sidewalks, bridges, and drainage channels.

Outdoor Lighting Systems (7 years): Light poles, underground wiring, and high-efficiency LED fixtures.

The IRS classifies parking lots, driveways, and drainage systems as land improvements with a 15-year recovery period under the MACRS system. Unlike the commercial building structure, which depreciates over a 39-year cycle, paving allows for much more aggressive amortization.

| Asset Type | Recovery Period | Standard Method |

| Building Structure | 39 Years | Straight-Line |

| Paving / Land Improvements | 15 Years | MACRS / Accelerated |

| Bonus Depreciation | 1 Year | Immediate Expensing |

A cost segregation study identifies and reclassifies specific property components to accelerate tax deductions, moving assets from a 39-year life to a 15-year life. By technically separating asphalt, curbing, and striping from the primary building cost, investors maximize the Net Present Value (NPV) of their tax savings. This strategy shields capital from tax erosion, allowing funds that would have gone to taxes to be reinvested into property operations or portfolio growth.

If the work restores the pavement to its original state (such as crack sealing), it is a deductible operating expense; if it is a total reconstruction, it must be capitalized as a land improvement. Capitalized improvements qualify for Bonus Depreciation, allowing a Capital Expenditure (CapEx) to be transformed into a massive first-year deduction. This distinction is vital for the Total Cost of Ownership (TCO), as well-managed asphalt acts as an active tax shield while preserving the physical integrity of the site.